There’s nothing like working on a plan for years only to be blindsided, pieces shuffled, strategies upended, and suddenly, you’re the one asked to leave. Aside from being quite a neat summary of life as a diplomat, it’s also what happened to Intel CEO Pat Gelsinger first thing Sunday morning.

Just before Thanksgiving, Gelsinger had officially secured a $7.9B grant from the Commerce Department to “supercharge American innovation” and “revitalise the US semiconductor industry,” a lift for the 56-year-old chipmaker that’s struggled in the face of fierce competition from Taiwan’s TSMC, America’s Nvidia, and Korea’s Samsung.

But then Gelsinger announced his resignation, leaving many asking an important question:huh?

Stay on top of your world from inside your inbox.

Subscribe for free today and receive way much more insights.

Trusted by 161,000+ subscribers

No spam. No noise. Unsubscribe any time.

When Gelsinger secured the top job in 2021, he laid out an ambitious five-year turnaround plan for Intel, including building new factories across the US and Europe to manufacture chips for other brands (not just Intel).

But five years is a long time in the stock market, and an eternity in the fast-moving semiconductor sector. So Intel’s board and investors grew impatient as — this year alone — Intel’s shares dropped 40% while rival Nvidia’s soared 200%. A post-Covid crash in the PC market had complicated Pat’s plans, and an $18B restructure to clear the decks didn’t seem to lift spirits — meanwhile, key board member Lip-Bu Tan’s resignation in August (just two years after being brought in to help) rattled markets further.

So the board gave Gelsinger a choice: retire or be removed. He went with option a.

Is this all Gelsinger’s fault?

The 68-year-old executive secured billions to set his plan in motion and placed his company at the heart of Washington’s efforts to revive America’s chipmaking capabilities (see below). But he was always working against two factors: i) time, and ii) politics.

First, this stuff is complicated and takes time: back in 2006, Intel was the first to make 45 nanometre chips (smaller = better), but it then got stuck trying to break past the 10nm barrier before hitting today’s 5nm. Meanwhile, TSMC is already pushing past the 2nm threshold – these gaps are physically infinitesimal, but they reflect years-long gaps in R&D.

And that all reflects just one of several poor decisions made years before Gelsinger even arrived — Intel was late to use ultra-advanced machines made by ASML in the Netherlands; late to pivot to smartphones; and then late to pivot to AI. And Pat’s chipmaker-for-hire play has racked up some serious losses as it’s struggled to close the gap.

Second, Gelsinger’s ability to play catch-up depended heavily on financing from the CHIPS Act, Biden’s effort to revitalise domestic semiconductor manufacturing. But that legislation could be at risk under Trump 2.0, with House Speaker Mike Johnson already flagging that Republicans could try to “streamline” it (he walked back earlier remarks about repealing it).

So does any of this really matter?

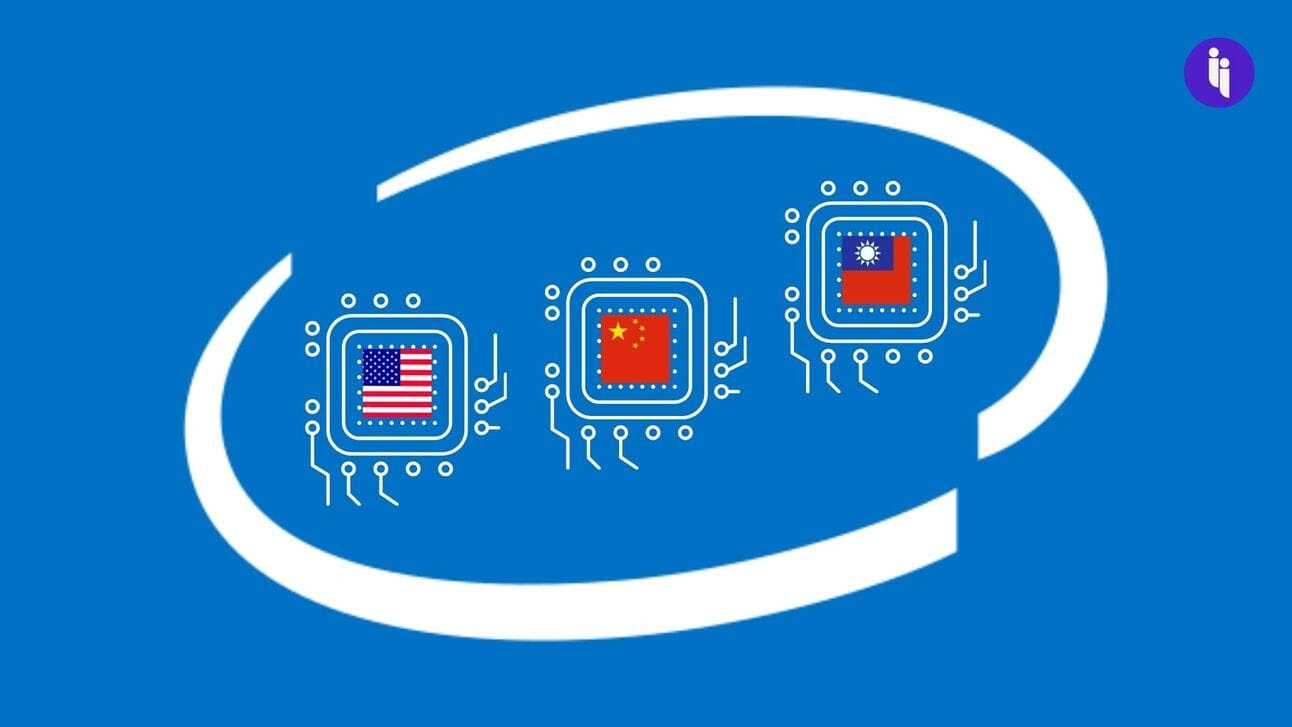

There’s a reason why the markets and Intel’s boardroom wanted Gelsinger to move faster, and why Washington was willing to hand him billions to help: the semiconductor industry will shape the 21st century — it helps power advances in just about every field of human endeavour, including defence and intelligence. And Intel is America’s main chip manufacturer (Nvidia, AMD, and Qualcomm lead in design but outsource manufacturing).

So what do Intel’s struggles mean for the US?

Well, the CHIPS Act’s three biggest bets were that America’s Intel, Korea’s Samsung, and/or Taiwan’s TSMC could help revive domestic chip-making in the US. But only one of the three is looking really promising at this stage: after a bumpy start with unions and other curveballs, TSMC’s vast and growing Arizona compound is now producing better results – and at a tiny 4nm – than back at HQ in Taiwan. And that’s surprised just about everyone, giving the whole venture a chance of surviving any curveballs under Trump 2.0.

So overall, the message seems to be that yes, the US can revive its ability to manufacture chips at home. But it’s going to involve a) some serious cash, b) some serious risk, and c) some serious (non-US) partners.

INTRIGUE’S TAKE

Intel’s story is gripping in part because of its role in US business mythology: its co-founder (Gordon Moore) just passed away last year, capping a life that not only coined Moore’s Law (the projection that transistor density would double every two years), but also ushered in Silicon Valley’s role as the innovation hub.

So when that company falls from a $250B market cap in 2020 to perhaps $100B today, it’s going to generate some reflection on America’s trajectory.

But there’s another side to the US business mythology, and you can see it in the guy who Intel opted not to buy out two decades ago, but who’s now personally worth more than all of Intel: that’s Jensen Huang, the founder of Nvidia. And his side of the US business mythology — the one the world is still figuring out how to emulate — is about America’s unusual capacity for continual regeneration.

Also worth noting:

- Intel is now worth ~$104B, while Nvidia is worth 30+ times more (~$3.4T).

- The Intel board has temporarily replaced Gelsinger with two co-CEOs: chief finance officer David Zinsner and executive vice president Michelle Johnston Holthaus. Intel shares jumped 3% on news of Gelsinger’s departure.

- Yesterday (Monday), Washington further tightened US export controls aimed at preventing China’s ability to produce advanced chips for its military.

- There’ve been rumours that Qualcomm (the US chipmaker more focused on cell-phones) is now exploring a possible purchase of Intel.